We often get asked what makes us different as tech investors. Our answer is our research, but it’s really the contrarian insights generated by our research.

Every well-read investor knows they must do things differently than consensus to generate returns better than the market. Although many accept the truth in these words, few investors have deeply considered what it means to be contrarian. Doug has spent the last several years deeply thinking about non-consensus thinking and how we can apply it at Deepwater. The result is what we call the contrarian mindset — a set of ideas and principles about what makes an idea non-consensus, and therefore, a potentially good investment.

In 2020, I wrote a book to teach myself how to think. It also defined how we at Deepwater think about investing and technology. The premise is simple: Only non-consensus ideas yield extraordinary results. A contrarian mindset is adopted by those who accept this premise and intentionally explore the non-consensus in pursuit of the extraordinary. Writing enables the deepest exploration of an idea, and a book creates a precise language and common concepts to understand an idea between author and reader. This piece aims to distill the language and concepts from my book into 1,500 short words to frame our future contrarian conversations.

The Core Concept: The non-consensus idea is the only way to achieve extraordinary results in anything.

Consensus is a general agreement among some group, the purpose of which is to shape group action around a common belief, resulting in a common outcome. The result in question may be good, even desirable, but anything common can only be ordinary.

The importance of non-consensus ideas is often cited in the investment world. By definition, if investors do the same thing as everyone else in the market, whether right or wrong, they will achieve average results. It is the job of professional investors to generate extraordinary results, otherwise the clients of those investors are better off just buying a low-fee market index.

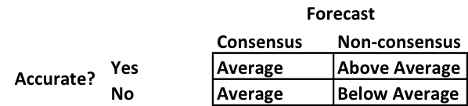

Howard Marks, a Mount Rushmore-level investing legend, explains the results of consensus vs non-consensus investment forecasts via a simple matrix:

But the power of the non-consensus idea isn’t limited to investing. The concept applies to all things in life, from entrepreneurship to creative pursuits to sports to politics. If you think or act the same way as everyone else, you should expect an ordinary result. That is the point of conventional wisdom.

Concept 2: Consensus forms around probability and acceptability.

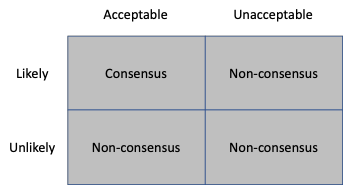

Consensus forms around two beliefs: probability and acceptability. Probability has to do with the group’s belief about the likelihood of a thing happening. Acceptability has to do with whether the group believes a thing should be allowed to happen or not.

Consensus about probability largely results in odds. Odds may be specific, as in the case of market prices or forecasts, or they may be abstract, as in the case of group instincts.

Consensus about acceptability largely results in rules. Rules may be specific, as in the case of laws, or they may be abstract, as in the case of social norms. Consensus accepts odds and adheres to rules by doing the things that seem likely and acceptable.

Probability and acceptability collide to offer us another matrix of where we find non-consensus ideas:

Concept 3: To be non-consensus, you must get uncomfortable by defying odds or breaking rules.

Only ideas that seem unlikely or unacceptable can be non-consensus. As a general rule, anything deemed unlikely or unacceptable by consensus should feel uncomfortable to support, if for no other reason than the idea diverges from the safety of the group. Conformists that stay with consensus enjoy guaranteed average results, even if the results are undesirable. Contrarians who diverge get terrible results if they’re wrong, but extraordinary results if they’re right.

Beyond the loss of group safety, contrarians are likely to suffer from ridicule, and in some cases anger, from the consensus herd for challenging the group, heightening the discomfort of considering non-consensus ideas. The benefit of contrarian discomfort is that few other people will try that non-consensus idea, at least until the idea is proven right. Then it becomes consensus.

Concept 4: There are 11 techniques for generating or identifying non-consensus ideas.

There may be more than 11, but these are the ones that seem most apparent to me, broken into the categories of unlikely and unacceptable.

The Unlikely

Unlikely ideas must defy odds and expectations to be non-consensus. Consensus forms predictions based on knowledge and data held by the group, so good unlikely ideas take advantage of knowledge and data missed or misinterpreted by the group.

The seven tactics to construct unlikely ideas are:

- Absurdum. Absurd or extreme ideas never seem likely to happen precisely because they are absurd or extreme. Anything that seems likely to happen cannot be absurd or extreme. Absurd ideas should seem ridiculous, silly, even stupid or laughable. Re-landing rockets to reuse on future space launches seemed ridiculous until it happened.

- Frankensteining. Frankenstein ideas combine two or more existing things to create a new and novel idea. Combining things unfamiliar to each other results in ideas unfamiliar to consensus, even more so when the ideas naturally oppose one another. A butcher that is also a hair salon. No one but a contrarian would ever consider such an idea.

- Echo. Echos borrow consensus ideas from groups outside of the one with which you’re trying to compete. A sports team owner may operate his business like a theme park or entertainment company, not a sports team. Jerry Jones, owner of the Dallas Cowboys, does exactly this. The Cowboys are the most profitable sports team in the world.

- Early Believer. New trends create non-consensus opportunities for early adopters if for no other reason than consensus has yet to form or even care. More often, consensus is actively skeptical of emerging trends because they are unfamiliar. Bitcoin has dealt with its fair share of skeptics, but it’s outperformed every stock- or bond-based asset class of the last five years plus. When consensus forms around new trends, it often results in outsized appreciation to the contrarians that adopt early. Skepticism can help avoid mistakes, but it can also prevent the extraordinary.

- Ingredients. Consensus often starts with an observation of some fundamental truth, but it becomes distorted over time as consensus focuses more on the finished product than the ingredients. Considering the ingredients of something breaks it down into its purest components, a sort of first principles thinking, allowing the contrarian to discover consensus misperceptions. Warren Buffet’s frequent wisdom comes from thinking about the ingredients of investing money well. One of his best is that investors focus on what a business will generate in terms of profit for shareholders. Speculators focus only on the share price of the business— where they buy and sell the asset. There’s a reason Buffet, and his disciples, consistently outperform the markets over the long term.

- Redo. When something has been tried before and failed, consensus assumes it will keep failing forever. It will always be non-consensus to attempt something that hasn’t worked in the past. The bigger the failure, the better. GM tried EVs before Tesla. Pets.com failed at online pet food before Chewy. Webvan blew up before Instacart and DoorDash.

- Remix. When something has been tried before and worked, sometimes it can be forgotten. A remix rediscovers an idea that worked before and updates it for the current time. Retro fashion, music, movies, and video games often come back into public consciousness, revitalized by a contrarian. SPACs are a recent remix in finance as an attractive way for tech companies to go public.

The Unacceptable

Unacceptable ideas must break (or create) rules. Rules exist to prevent an otherwise likely thing from happening, so acting on unacceptable ideas demands an acceptance by the contrarian of some punishment, whether legal or social.

The four tactics to generate unacceptable ideas are:

- Robin Hood. Robin Hood stole from the rich to give to the poor. The Robin Hood contrarian does the same by breaking the rules on behalf of some unorganized group in need or want. Airbnb made it easy for people to rent apartments to travelers, damn the zoning laws.

- The Heel. In professional wrestling, the heel is the bad guy. His job is to intentionally draw heat (anger) from the crowd by intentionally offending it. The contrarian heel’s goal is the same. To be intentionally offensive requires breaking consensus rules and results in attention, making it a strong strategy for media and entertainment endeavors. Howard Stern and Barstool Sports are classic heels. So is Donald Trump.

- Rational Bad Guy. Irrationality and hypocrisy often corrupt consensus beliefs. The rational bad guy enforces reason against inappropriate rules where consensus willfully fools itself about the acceptability of something, whether out of ignorance or intent. Whereas the heel plays the bad guy for attention, the rational bad guy does it in the name of truth and rationality.

- Moral High Ground. In the moral high ground strategy, the contrarian attempts to establish or formalize some new rule by illuminating its virtue to the crowd. Done effectively, consensus melds around the idea, anointing the contrarian the heir to it. Dove set the bar for body positivity with its Real Beauty campaign almost 20 years ago, a mantle it still holds today.

Conclusion

Contrarians live with two mandates:

- Explore the uncomfortable, which is whatever seems unlikely or unacceptable.

- Be right, whether in conformity or dissent.

The four concepts explored here deal with exploring the uncomfortable reality of the unlikely or unacceptable idea, but being right is equally important. Contrarians lose big when they’re wrong and, as Jeff Bezos notes, contrarians are often wrong. But when they’re right, the results are extraordinary.