We recently shared these thoughts with our limited partners about current public market dynamics.

When someone asks if we’re in a market bubble, the expectation is for one of three answers:

- No

- Yes, but it isn’t ready to pop

- Yes, and it’s ready to pop any minute

But the answer is rarely so simple. Here’s what we think: There are certainly some pockets of the market exhibiting bubble-like behavior, driven by retail speculation, but who knows when they’ll pop. As to whether the entire market is in a bubble, there seem to be some signs that warrant caution, although signals are mixed. Overall valuations are elevated relative to historical norms, but interest rates are also at historical lows and fiscal stimulus appears open ended. The real point of asking whether we’re in a bubble is figuring out what to do if we are, or even if we aren’t. Either way, we think now is a good time to play offensive defense.

We offer three observations from our study about the bubble question, one about the evidence of a bubble, one about risks to the market, and one about opportunities to play offensive defense.

Evidence: What makes a bubble?

Our research tells us there are three core components to a bubble: leverage, a captive public imagination of rapid riches, and the resultant extreme valuation of some asset class.

Leverage played an obvious factor in the 2008 financial crisis driven by aggressive home lending and securitized debt products that masked risk. It also played a factor in the dotcom boom in the form of margin. Calls on margin accounts helped burst the bubble when the market finally turned. The same borrowed money to purchase equities factored into the 1929 crash. Where we find egregious leverage, we often find the breadcrumbs that point to a bubble.

So, where is the leverage today?

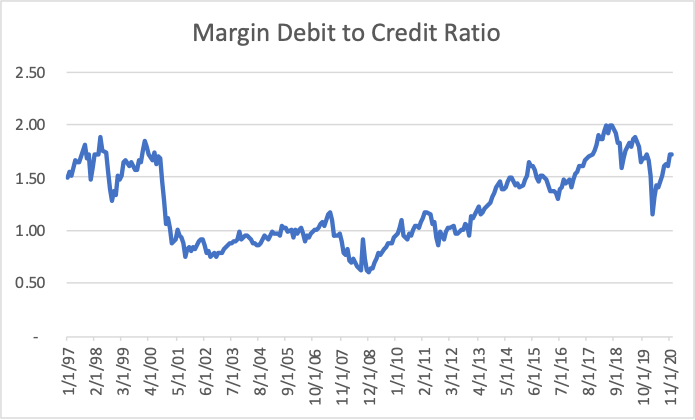

Consumer debt ratios are near 40-year lows. Corporate debt, which has expanded aggressively in a low interest rate world, seems to have had to most expansion in leverage at the highest-quality companies. If anywhere, it seems the leverage factor could again come in the form of margin. FINRA data tells us margin levels are at all-time highs with balances of $778 billion on margin as of December 2020, but these numbers need more historical context. A better way to assess margin may be to consider the amount of margin in the system divided by the free credit balances (cash accounts and cash balances in margin accounts). When considering this ratio, which was 1.72 in December 2020, we can see that margin is still at elevated levels relative to history, although it’s been at those levels for the last several years.

After periods of financial distress, like the dotcom bust and the 2008 financial crisis and even the beginning of the pandemic, margin levels decline drastically relative to cash balances. Our current margin levels are more in the realm of those during the dotcom boom, but we also have historically low interest rates, creating low hurdles for return on margined investments. Interest rates will be a recurring theme as we assess the evidence of a potential bubble, and they make it hard to say whether current margin levels are a real danger or just a byproduct of the availability of cheap money.

After leverage, the next core ingredient of a bubble is euphoric participation from the broader public. Bubbles aren’t bubbles until the public gets involved because a bubble requires a universal psychology of excitement and maximal financial participation to inflate asset values. The pandemic has certainly brought the retail investor into the market, helped by the move of most brokers to offer commission-free trading. Citadel has said retail trading now makes up 25% of market volume some days and averages 20%, which compares to just 10% in 2019.

In the tech space where we traffic, it seems retail investors have the strongest influence in the electric vehicle trade, new IPOs, SPACs, and short duration options. We’re also seeing more recent activity from retail investors short squeezing highly shorted stocks like GameStop and Blackberry.

Anywhere retail investors exert extreme influence gives us pause. Retail investors always seem to be willing to pay higher valuations for companies that appear to have massive growth opportunities, usually because retail investors tend to speculate more than they invest. Retail investors may be right about some of the companies they’ve bid up, but it makes the mandate for growth all the stronger if an investor wants to generate an extraordinary long-term return based on the company’s actual business prospects. Given the ugliness we’ve seen around short selling, it seems best to avoid retail mania as a whole, unless you can get in beforehand, and look for opportunity elsewhere.

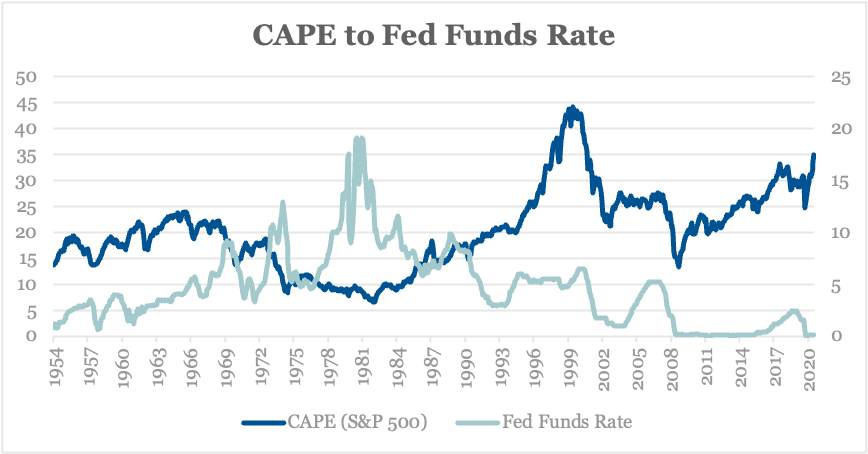

Leverage plus retail brings us to the final piece of data in exploring the question of a bubble: market valuations. It’s true that P/Es are at elevated levels relative to history. Robert Shiller’s CAPE (cyclically adjusted P/E) for the S&P 500 is at 35. The only other times we’ve seen a CAPE above 30 were in 1929 and during the 2000 dotcom bust. If we look at forward multiples across large to small cap stocks in the U.S., we will find a similar story of historically high valuations. However, we also have historically low interest rates — zero, for example, compared to ~5% in 2000 — which support higher valuations for equities.

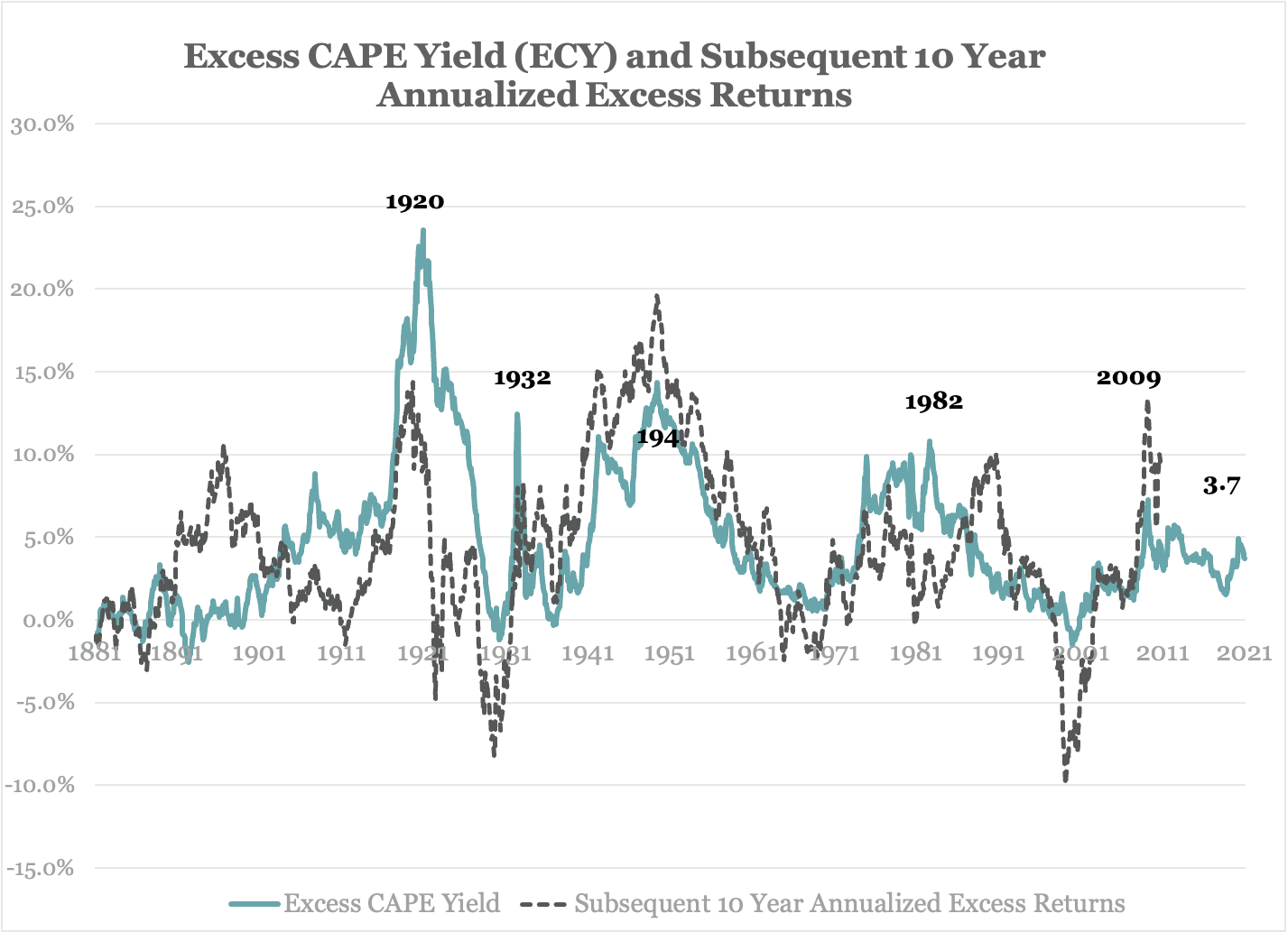

Even Robert Shiller himself has argued that equity valuations may not be as inflated as they appear on the surface when factoring in low interest rates and inflation via his Excess CAPE Yield metric (ECY). Considering this measure, the market valuation picture looks quite different from the 1929 and 2000 crashes. In each of those certain bubbles, ECY was negative and corresponded with negative annualized 10-year returns. Today, ECY is 3.7%, which is roughly in line with the median value of ECY going back to the 1880s of 3.5%.

Risk areas

We think there are two main risk factors that could represent negative catalysts to the current market environment, bubble or not: inflation and corporate taxes. Logic would suggest that if the government pumps enough fiscal stimulus into any system, eventually it should create some level of inflation. To date, inflation hasn’t been an issue. If inflation did become an issue, and it stayed meaningfully above the Fed’s ~2% target for some period of time, it would necessitate increasing interest rates, which would likely result in a rerating of market valuations. However, inflation is impossible to predict, and we aren’t going to try.

An increase in corporate taxes seems easier to predict, although the market doesn’t seem to be predicting it. President Biden made it clear in his campaign that he intended to raise the corporate tax rate from 21% to 28%. It seems reasonable to assume that a tax increase ultimately happens given Democrat control of the three branches of government, and the ability to use reconciliation to pass the bill. Despite this seeming reality, consensus S&P 500 earnings are expected to grow 16.6% in 2022 to $195.51 after growing 23.4% in 2021 to $167.61 as we come out of the pandemic. S&P 500 earnings were $162.97 in 2019 pre-pandemic and expected to total $135.79 in 2020 (-16.7% y/y).

Given 2022 estimates, either the market isn’t factoring in the likelihood of a corporate tax increase being passed this year, or it is and therefore must expect underlying earnings growth of something more like 25% y/y in 2022. The latter scenario seems unlikely. In 2018, we saw nearly 23% y/y reported earnings growth in the S&P 500, and that was after President Trump’s corporate tax cuts. Twenty-plus percent earnings growth for the S&P 500 is the exception that happens coming off of recession periods, like in 2020, or after tax cuts, like in 2018.

The bottom line on taxes: If the market eventually factors in a more realistic 2022 earnings situation, which may be more like up mid-single digits from 2021, then the market could justifiably pull back 10% assuming a stable multiple.

Opportunity areas: offensive defense

We see four opportunities to play offensive defense:

- Transformative tech. We always focus our investment efforts on companies creating truly transformational products that offer positive long term DCF valuations and are led by contrarian management. These companies are extremely rare to find, but we believe they offer insulation from wild markets in that even in a pull back, these companies will be seen as long-term winners and recover quickly as the market recognizes their true potential. That doesn’t mean these companies are a good investment at any valuation, but often the best tech companies are good investments at valuations that seem uncomfortable based on conventional wisdom. Investing in things that feel comfortable in tech probably means it’s a consensus idea, which probably means that it doesn’t offer the potential for extraordinary returns.

- International tech. Internationally listed tech stocks as a whole haven’t seen the same level of run as US tech stocks, likely given less exposure to US retail investors. We think there are some opportunities to acquire shares in select international tech companies with transformative potential at valuations that appear attractive based on both near and long-term expectations.

- Hidden tech. Hidden tech stocks, like internationally listed ones, also haven’t seen the same level of retail speculation as obvious tech. Hidden tech companies are legacy companies, maybe not even tech companies, that have developed some new technology that’s allowing them to build into a massive new market. These stocks may be considered “value,” but hide an underlying growth mentality. One of our favorite hidden tech stocks that isn’t so hidden any more has been Axon. The company is better known as the maker of Tasers, but also makes body cameras and software for law enforcement agencies, which is the company’s fastest growing business. Companies with hidden tech that have yet to be valued like tech companies are a strong offensive defense play in this market.

- New SPACs with underappreciated sponsors. Due to the structure of a SPAC, downside is limited to the issue price of the stock. If the SPAC either fails to make an acquisition or makes an acquisition the investor doesn’t like, the issue price is returned to the investor. In the absence of investing at the offering of a SPAC with strong sponsors (the best case), investors may also find asymmetric upside by investing in SPACs near deal price with underappreciated sponsors, preferably associated with private market tech investing.

Whether we’re in a bubble or not, it’s never popular to make a call about a market slowing down where investors can’t help but see asset values climbing, particularly in tech. The Nasdaq was up 29% or more three of the last four years. While we think it’s unlikely that the market offers that level of performance for the next four years, we do think there are pockets in tech that will offer those types of strong returns in the future. Now, more than ever, investors need to rely on active management to find those transformative opportunities.