skip to Main Content

Products

Insights

Philosophy

Analysis

Team

Search

Search

Submit

×

Close search

Apple

Gene Munster, Brian Baker

India Is Starting to Help Apple Diversify Its Production

Apple's dependency on China keeps investors up at night. Today Deepwater estimates that 40-45% of Apple's overall revenue is manufactured in China, and expects that to decline to 25-30% in five years. We believe half of the decline will be the direct result of production moving to India.

Read More

Apple

Gene Munster, Brian Baker

iPhone 15 Upgrade Experience Underscores Apple Is a Consumer Staples Company

Apple excels at making consumer tech easy to use. The most recent example is the streamlined iPhone setup experience. Doing the little things right is why consumers who own one Apple product purchase additional products, locking those users in as lifelong customers.

Read More

Apple

Gene Munster

iPhone 15 Is Enough to Return Apple to Growth

Apple’s fall hardware event featured the new iPhone 15 family and updates to Apple Watch at prices unchanged from a year ago. While most of these updates were incremental, they’re enough to attract the 400m iPhone owners with phones more than 4 years old, which should return Apple to revenue growth in the December quarter. Most impressive was the addition of spatial photo and video capability on iPhone 15 Pro models, which lays the foundation for Vision Pro demand, due out early next year.

Read More

Apple

,

Spatial Computing

Gene Munster

iPhone China Ban Is Largely Immaterial

Shares of AAPL have recently declined by about 3% based on investor concern that an expanded iPhone ban for Chinese government employees and its affiliated companies will dampen Apple's sales. My math suggests the worst case scenario is a 1% negative impact on Apple's overall revenue in 2024. The bigger question is what's the long-term impact of the US and China moving in a different direction? The answer: Softness in China can be offset by strength in India.

Read More

Apple

Gene Munster

Apple’s App Store Is an Important Part of Its Profitability — And It’s Not Changing

The Supreme Court rules that Apple does not have give developers the option to steer payments outside of the App Store. That means that status quo of the App Store business model which should generate about 20% of the company's operating income this year is intact. The ruling also keeps Apple one step ahead in Washington's pursuit of big tech regulation.

Read More

Apple

Gene Munster

Apple Setting up for Faster Growth in December

Shares of AAPL traded down 2% after posting what was essentially an in-line June quarter. Guidance for September calls for a 1% y/y decline in revenue compared to expectations of 1% growth. Those details water down the most important dynamic of the quarter: the installed base of active devices hit an all-time record. That means Apple's ecosystem is expanding which is key for long term investors. This growing base should power revenue growth acceleration in December and for full year 2024.

Read More

Apple

Andrew Murphy, Gene Munster

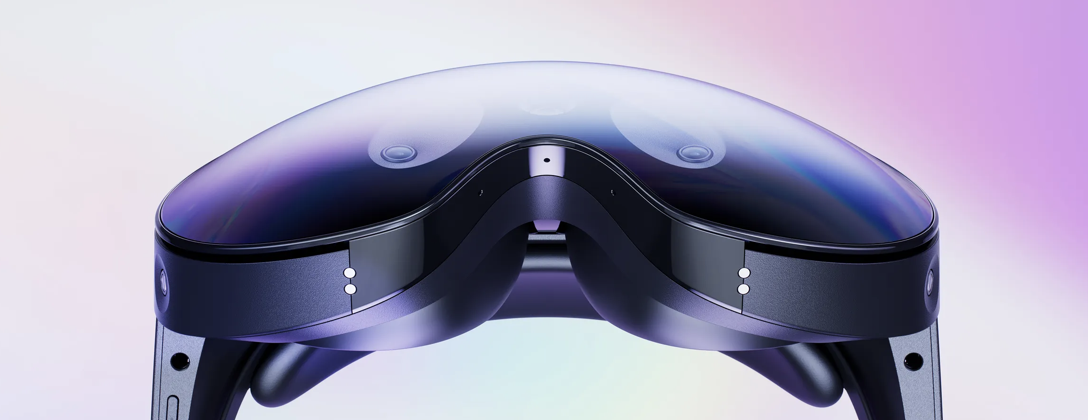

Vision Pro Demo Review: Open-Ended Potential

At Deepwater, our mission is to profit from where the world is going. This week, Gene got a preview of that future with a demo of Apple’s Vision Pro mixed reality headset. In this episode of Deepwater TV, Andrew and…

0-Minute Read

Apple

,

Spatial Computing

,

Virtual Reality

Gene Munster, Andrew Murphy

Apple Vision Pro’s Spatial Computing Is a Big Deal

Apple made good on the rumor mill, announcing its first spatial computing headset, Apple Vision Pro. Available in early 2024 and priced at $3,499, it is at least $500 more expensive than most were expecting. The keynote left me with more questions than answers. After an hour-long demo my view of the product expanded. Spatial computing is a big deal. Yes, it's very expense and, yes, the selection of apps will be limited early on — but those barriers will disappear over time. Spatial computing is just too powerful not to go mainstream. I believe it will account for 10% of all Apple sales in 2030.

Read More

Apple

,

Augmented Reality

,

Spatial Computing

,

Virtual Reality

,

Wearables

Gene Munster

Meta and Apple Can Will AR Into Reality

0-Minute Read

Apple

,

Meta

,

Themes

Gene Munster

Headsets Mean Little to Apple in the Near Term but a Lot Over the Long Term

It's been eight years since Apple jumped into a new product category. On June 5 that will likely change when Apple is expected to preview its $3,000 developer version of a mixed reality headset at WWDC. Many investors are skeptical about the prospects of the device given headsets are currently a solution looking for a problem. I believe the trend of more immersive consumer tech experiences will continue, which should pave the way for a robust headset market. By 2030, I believe the wearables/glasses segment could account for 10% of Apple's sales (assuming they don't release a car), a business similar in size to Apple's Mac and iPad businesses today.

Read More

Apple

,

Themes

Gene Munster

For Apple, It’s All About the Active Device Base

For the March quarter, Apple beat estimates and guided revenue slightly below the Street for the June quarter. Despite the soft guide, shares of AAPL traded up 2% in after-hours. I believe the stock's strength is evidence that investors are putting more weight on Apple's active device base which grew in the quarter to over 2B despite products revenue being down 5% y/y. A growing base means the Apple product flywheel is working which is the foundation for the Apple investment case to shift to a consumer staples company that should yield a higher multiple. On top of that, AI and India represent untapped opportunities for the company.

Read More

Apple

,

Themes

Gene Munster

Apple Preview: The Only Consumer Staple With AI Upside

Apple reports March results on May 4th. Outside of the typical focus on iPhone and Services revenue and guidance there will be increasing attention on the company's active installed base, which grew 8% y/y in the Dec-22 quarter. A growing base means the Apple product flywheel is working. That base is the foundation for the Apple investment case to shift to a consumer staples company that should yield a higher multiple. On top of that, Apple is making meaningful progress in AI, a dynamic that is under-appreciated by investors.

Read More

Apple

,

Themes

Load More

Back To Top

Search

Submit